What Is Recoverable Depreciation? A Simple Guide for Homeowners

When a storm damages your roof or a pipe leak ruins your flooring, navigating an insurance claim can feel overwhelming. One of the most confusing parts for homeowners is something called recoverable depreciation.

If you’ve ever looked at your insurance paperwork and wondered why your claim is split into different payments or why the insurance company is “holding back” money, this blog explains everything in simple, clear terms.

✔️ What Is Depreciation?

Before we explain recoverable depreciation, it helps to understand depreciation. Depreciation is the amount of value your property loses over time as it ages. Just like cars lose value the moment you drive them off the lot, roofs, floors, siding, and other home components lose value the older they get.

Insurance companies look at:

The age of the item

The expected lifespan

Its condition before the loss

Then they subtract that amount from the total claim. This “subtracted” amount is called depreciation.

✔️ So What Is Recoverable Depreciation?

This is where it gets easier:

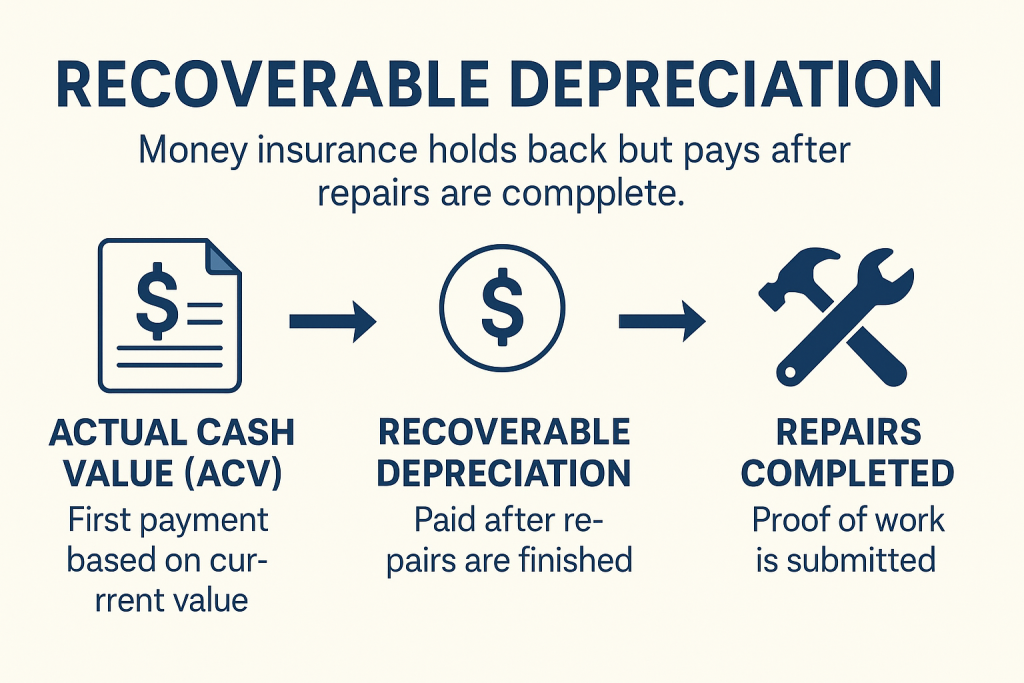

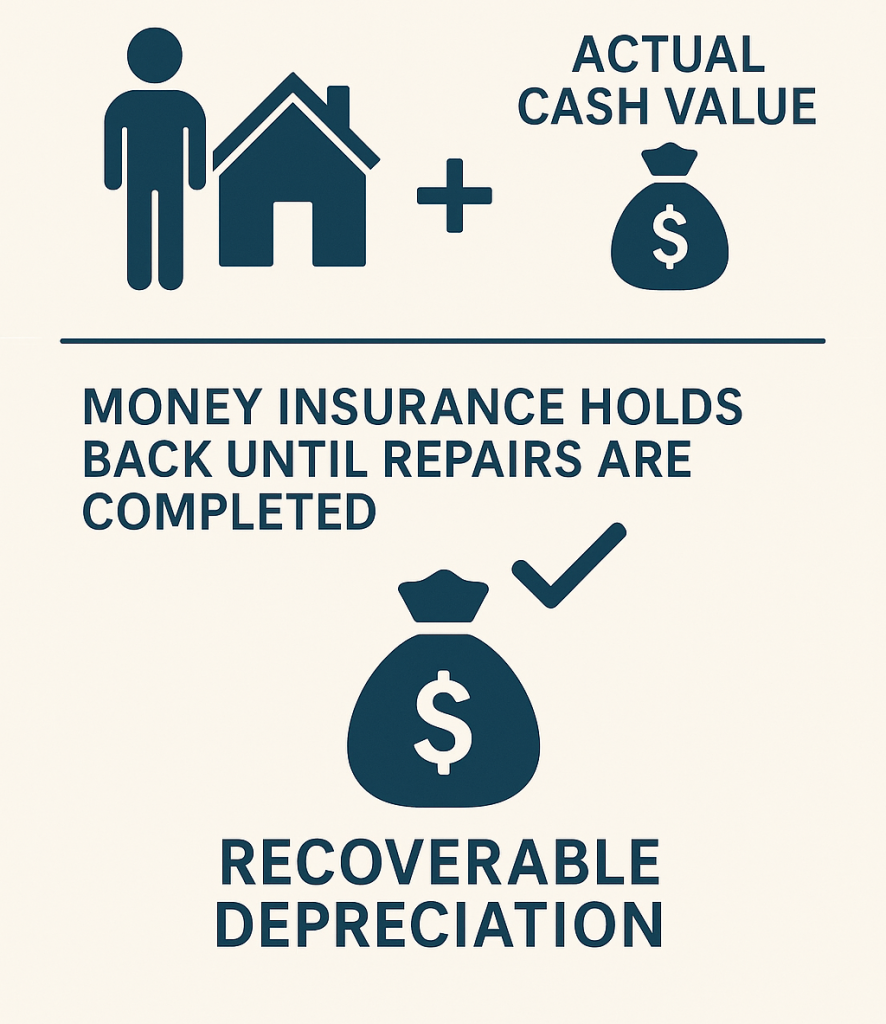

Recoverable depreciation is the money the insurance company holds back, but gives you AFTER the work is completed.

Think of it as the second half of your claim.

First payment: Actual Cash Value (ACV)

→ The value of your damaged item today, after accounting for age/wear

Second payment: Recoverable Depreciation (RCV Holdback)

→ The amount you get back once the repairs are finished

✔️ Why Does Insurance Hold Back Money?

It’s a common question:

“Why don’t they just pay everything upfront?”

Here’s why:

1. To ensure the repairs actually get done

If the insurance company paid the full amount upfront, some homeowners might pocket the money and skip the repairs.

2. To prevent fraud and inflated claims

By releasing the final funds after work is completed, insurance companies verify:

The damage was repaired

The repairs cost what was estimated

No extra funds were taken unnecessarily

3. To comply with Replacement Cost policies

With Replacement Cost Value (RCV) policies, homeowners are entitled to the full cost of repair, but only once the repair or replacement actually happens.

✔️ The Easiest Way to Understand It (Kid-Level Explanation)

Imagine your child breaks a toy.

A parent might say:

“I’ll give you part of the money to get a new toy now, and once you actually go buy it, I’ll give you the rest.”

Insurance does the same thing:

They give you part of the money now (ACV)

They give you the rest after repairs (recoverable depreciation)

It’s that simple.

✔️ A Real-World Example

Let’s use a roof claim:

New roof cost: $12,000

Insurance decides your old roof had $4,000 of depreciation

You receive:

$8,000 ACV (first payment)

$4,000 recoverable depreciation (second payment after roof is replaced)

Once the contractor finishes the job and the final invoice is sent, insurance releases the remaining $4,000.

✔️ How Do You Get Your Recoverable Depreciation Released?

Most insurance companies require the following:

Contractor’s final invoice

Photos of completed work

Sometimes a certificate of completion or signed statement

Your contractor (like us) typically handles the documentation and submits it on your behalf.

✔️ Final Thoughts

Recoverable depreciation can sound intimidating or confusing—but once you understand the concept, it’s straightforward:

**It’s money held back until repairs are done.

Finish the work → send proof → receive the rest.**

If you’re a homeowner dealing with storm damage or an insurance claim and need help understanding your estimate, we’re here to guide you through the entire process, step-by-step.